Key takeaways:

- Management Liability (ML) Insurance covers directors and officers against the exposures & risks that come with managing a business.

- An ML policy protects you and your business against things like: OH&S dramas, harassment, defamation, fines, fraud, theft and data breaches.

- ML claims have increase 300% over the last 5 years, with the average penalty awarded against companies costing $62,000.

There are a multitude of risks facing small businesses in Australia’s challenging economic environment today. New and often complex legislation are always on the horizon where companies can also expect increased exposure to liability and fraud.

“As a business owner, you automatically take on the risk of being personally liable for the consequences of any unintended errors arising from your own daily actions, or even the actions of your employees”.

The changing regulatory environment in Australia has increased the operating risks for businesses of all sizes – workplace accidents are now subject to high statutory scrutiny; employee theft is on the rise, while employment and commercial disputes are becoming more and more expensive to resolve.

If you’re a business owner, director or senior manager/officer of a private company, you automatically take on the risk of being personally liable for the consequences of unintended errors arising from your own daily actions, or even the actions of your employees.

Why should you invest in management liability insurance?

Irrespective of industry or company size, without adequate protection you could risk losing not only your business, but also your personal assets – such as your home – from being sold to cover the cost of paying claims. This insurance protects you personally, and therefore your wealth and lifestyle.

Claims can also be brought against directors and officers from every angle. Disgruntled shareholders, customers, investors, employees, competitors, regulators and creditors all have a legal entitlement to launch action if they feel directors and officers have not lived up to their responsibilities.

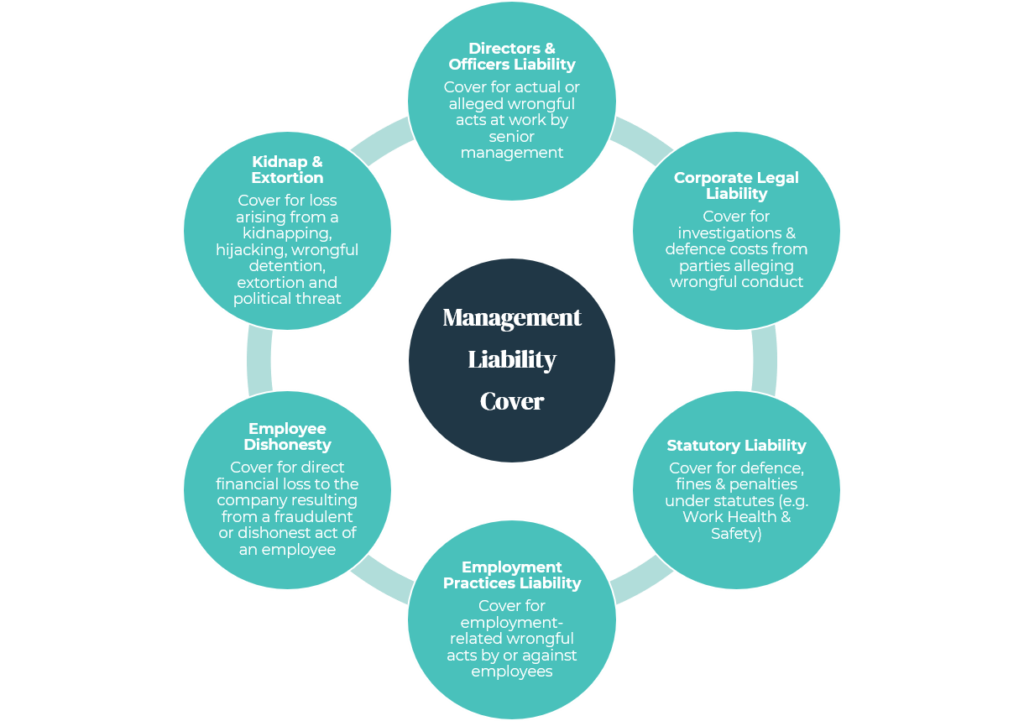

What can a Management Liability policy cover you for?

The three most common management liability claims are for employment practices such as bullying, harassment and wrongful dismissal. But ML covers a range of risk exposures affecting directors and officers of private companies.

“Claims can be brought against senior management from every angle, including disgruntled shareholders, employees, customers or competitors”.

Many businesses think it won’t happen to them, but statistics show otherwise.

Management Liability insurance claim examples:

- A customer database was illegally breached, and personal information was compromised. The costs of advising the customers plus the legal representation were covered by their ML policy.

- A manufacturing employee manipulated the accounts payable system to create non-existent customers and generated purchase orders and invoices to transfer money to the fake accounts, by accessing other employee authorisation details. An internal audit eventually discovered the total losses.

- A senior employee is dismissed after lodging complaints of bullying and aggressive conduct by the managing director. Complaints are also made of racial discrimination and disability discrimination. Action is commenced in the Federal Court and the matter is settled for a 6-figure sum.

Who can bring an ML claim against a company, its directors, officers and employees?

- Regulators (e.g. ACCC, ASIC, the ATO)

- Employees

- Competitors

- Creditors

- Shareholders

- Clients

- Liquidators/Administrators

What usually isn’t covered in the policy?

Generally, the policy won’t cover cyber-crime (unless specifically set out in your policy), employee entitlements, property damage or bodily injury. There may be other exclusions included in your policy which your broker can outline for you.

Without Management Liability insurance, you become exposed to significant financial loss, disqualification from your position, or even bankruptcy. With such penalties, it shows there is a clear need for an effective way to protect your business.

So why take even the slightest chance of putting your business or personal assets at risk? ML cover can provide you with peace of mind, leaving you to focus on what you do best.

DISCLAIMER:

This article is informational only and should not be construed as individual advice as it does not consider your individual needs. You should consider if the insurance is suitable for you and read the Product Disclosure Statement or policy Wording before buying insurance.

Leave A Comment